Collections Voice AI: Designing Promise-to-Pay as an Approval Gate

Collections and past-due reminder calls should not start with “how many calls can AI make?” The safer question is where the AI must stop. If a system cannot distinguish a payment intent from a dispute, hardship signal, or approval-required exception, it becomes an operational risk rather than a recovery tool.

Collections Calls Are State Decisions, Not Persuasion Scripts

A standard appointment call has a narrow path: find a time, confirm it, and write it back to CRM. A collections call has a wider state space.

- Basic payment intent

- Request for a different payment date or partial payment

- Dispute about the debt or amount

- Sensitive hardship signals such as health, family, or financial distress

- Expressions that require advisor, compliance, or legal review

The best collections automation is not the AI that pushes harder. It is the AI that knows exactly when to stop.

The U.S. FDCPA separates areas such as harassment or abuse, false or misleading representations, unfair practices, and debt validation notices. Local implementation needs legal review in each market, but the operating lesson is portable: teams need evidence of what was said, why the AI continued, and why it handed off.

Promise-to-Pay Is an Approval Gate

Promise-to-Pay (PTP) is the moment a customer says they will pay a certain amount by a certain date. That moment should not be stored as a loose note. The voice agent should structure the commitment, check policy conditions, and route exceptions to a human before the promise is treated as confirmed.

Voice AI decision states

1. inform_only : basic notice and allowed information

2. ptp_candidate : payment date/method needs confirmation

3. approval_required : dispute, hardship, sensitive or exception condition

4. human_handoff : advisor connection or scheduled callback

This makes the operating boundary visible: the AI did not “collect.” It processed the call up to a defined state and escalated the rest.

The Operating Loop: From Customer Language to CRM Evidence

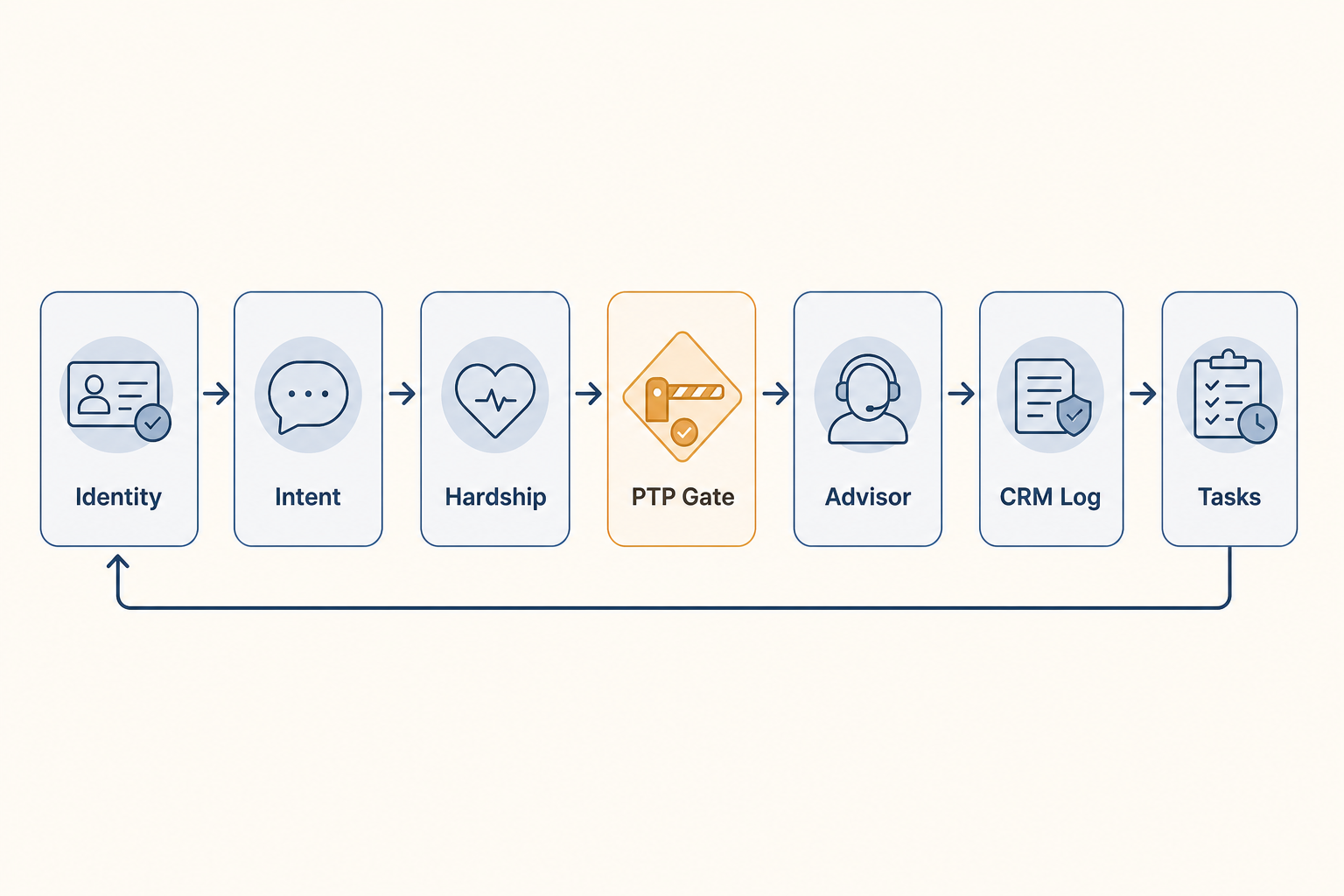

The diagram below shows the minimum loop for a collections Voice AI workflow. The end of the call is not the end of the process; the durable output is CRM evidence and the next action.

- Identity check: verify the customer with the minimum necessary account cues.

- Intent and situation detection: distinguish payment, reschedule, dispute, and hardship signals.

- PTP gate: structure date, amount, payment method, and customer confirmation.

- Advisor approval: stop auto-confirmation when exception or sensitive conditions appear.

- CRM writeback: log

intent,ptp_date,ptp_amount,risk_flag,handoff_reason, andnext_action.

Advisors Need Fewer, Better Fields

Collections teams often fail not because they lack data, but because the useful signal is buried in call notes. Advisors should see a compact control record first.

| Field | Purpose |

|---|---|

verified_identity | confidence level of customer verification |

customer_intent | pay, dispute, delay, or advisor request |

promise_to_pay | structured date, amount, and method |

hardship_signal | sensitive or vulnerable-customer signal |

compliance_flag | dispute, prohibited language risk, or exception |

next_action | SMS, advisor callback, hold, or close |

With these fields, managers can review the safety of automation before they optimize recovery volume.

BringTalk POV: Stop Logic Comes Before LQA

BringTalk’s LQA and FUA patterns are useful because they turn a conversation into a structured next action. In collections, the same pattern should be constrained by Stop Logic before scoring or follow-up automation.

- If the customer shows payment intent, structure it as a PTP candidate.

- If a hardship signal appears, do not confirm without advisor approval.

- If the customer disputes the debt, switch from recovery scripting to validation handling.

- If follow-up is needed, schedule it through FUA with approved message rules.

The KPI is not only containment or automation rate. Collections Voice AI should be judged on correct stopping, evidence quality, and next-action accuracy.

Pre-Launch Checklist

- Are prohibited phrases and approval-required conditions defined as policy, not just prompt text?

- Is PTP stored as structured data rather than free-text notes?

- Does the system stop auto-confirmation when dispute or hardship signals appear?

- Does CRM show the next action, owner, and reason?

- Does QA review state transitions, not only call recordings?

Collections automation is not about making more calls. It is about safely converting customer language into

state → approval → evidence → follow-up.

Public Sources Referenced

- FTC, Fair Debt Collection Practices Act text: https://www.ftc.gov/legal-library/browse/rules/fair-debt-collection-practices-act-text

- Cornell LII, 15 U.S.C. §1692d Harassment or abuse: https://www.law.cornell.edu/uscode/text/15/1692d

- Cornell LII, 15 U.S.C. §1692e False or misleading representations: https://www.law.cornell.edu/uscode/text/15/1692e

- Cornell LII, 15 U.S.C. §1692g Validation of debts: https://www.law.cornell.edu/uscode/text/15/1692g